State of the North American Airline Industry

Is the Industry Finally Seeing a Smoothing of the Boom/Bust Cycle?

By ALPA Economic & Financial Analysis Department Staff

The latest North American economic and financial information indicates that airline profitability should continue for the ninth consecutive year. Years of profits are due, in part, to various airline initiatives that include more agile responses to macroeconomic changes, investing in more fuel-efficient aircraft, focusing on enhanced ancillary revenue products, strengthening balance sheets, and improving operations. After a lengthy period of industry profits and with the economy experiencing some of its strongest growth in years, many are wondering if the industry is strong enough to weather the next downturn. With one of the most well-respected stock investors in modern times now owning shares in four major airlines, it seems as if the airline industry is indeed more attractive as a long-term investment option. Not only have stockholders seen improved returns from the airline industry, but many employees have also reaped the benefits of pattern bargaining resulting from sustained profitability.

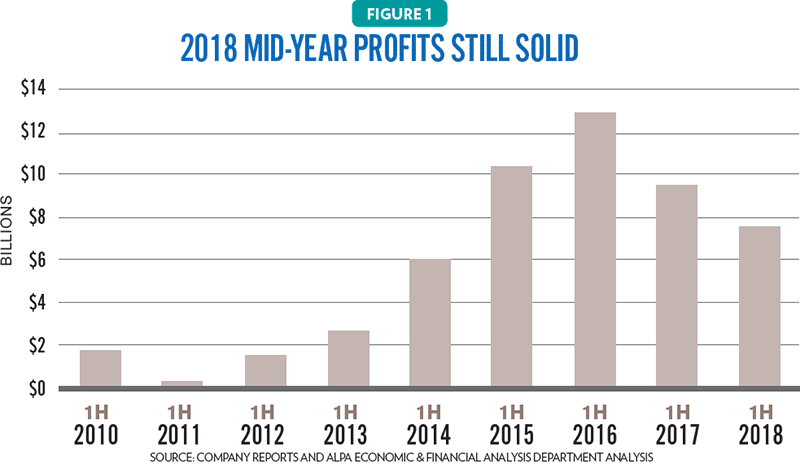

At the midpoint of 2018, major passenger airlines in the U.S. have earned more than $7.5 billion in pretax profits while major cargo airlines have gained more than $6.5 billion. Major Canadian airlines have earned nearly $500 million in operating profits. The unique business model at fee-for-departure airlines has contributed to these airlines having mixed results (see Figure 1).

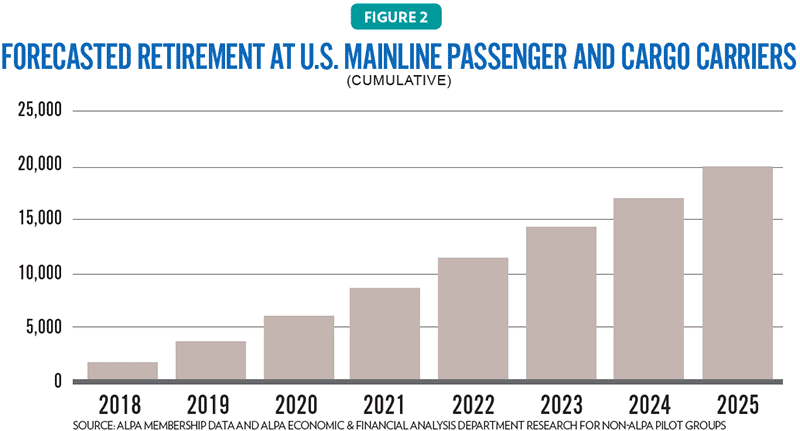

While these profit figures are significant, the industry continues to face varied macroeconomic and industry-specific challenges, which means that the concept of booms and busts can’t be discounted. Trade protectionism and rising fuel costs are two of the top challenges the industry faces in the near term. In the medium term, the industry could struggle with pilot supply (see Figure 2). And over the long term, the airline industry could face pressure from infrastructure constraints. Despite all these challenges, the airline industry is expected to produce profits for the remainder of 2018 and into 2019.

Much of the reason for the profitable outlook is the economic environment. General economic trends are positive both in North America and globally. U.S. real gross domestic product (GDP) rose 4.2 percent in the second quarter, driven by strong consumer spending and business investment. Economists expect the solid growth trend to continue, with full-year 2018 GDP growing 3.0 percent. If this materializes, it would be the biggest increase in GDP since 2005.

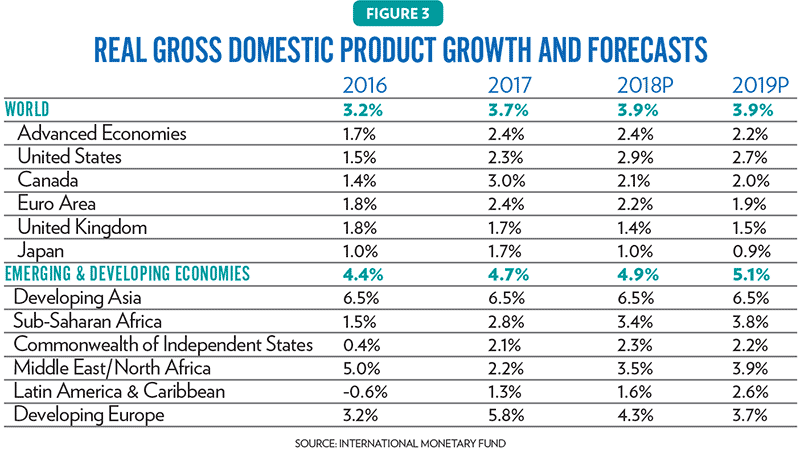

The International Monetary Fund predicts that world GDP will grow 3.9 percent in both 2018 and 2019. Canada’s GDP is expected to increase 2.1 percent in 2018, while Mexico’s output will grow 2.3 percent. Growth in the EU and Japan is expected to slow, while Asia’s growth should average 6.5 percent. China’s growth will moderate from 6.6 percent to 6.4 percent, and India’s growth rate will be 7.3 percent. Latin America will see modest growth of 1.6 percent in 2018, moving toward 2.6 percent in 2019. Both Argentina and Brazil have seen moderate currency depreciation as recovery in these areas has slowed and political tensions have risen (see Figure 3).

Trade tensions are beginning to present some downside risk to the global economic outlook. Besides already impacting the stock markets, increasing restrictive trade measures could hinder investment, as businesses wait to see what other products and goods could be affected. In recent months, the U.S. has imposed tariffs on steel, aluminum, washing machines, solar panels, and a variety of imported goods from China, including aircraft maintenance parts. In addition to the new tariffs between the U.S. and China, among others, the North American Free Trade Agreement (NAFTA) is being renegotiated, as are the economic arrangements between the UK and the rest of the EU. Many economists agree that the slowing of tradable goods causes inflation, slows the spread of new technologies, and could lower productivity.

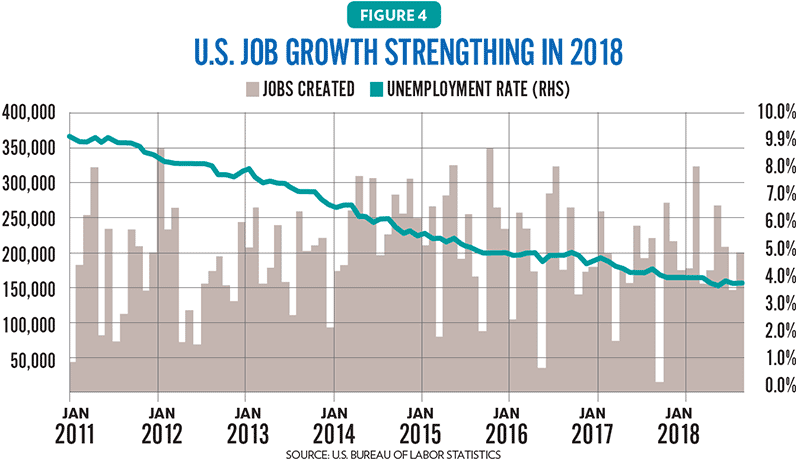

Despite all the recent trade headlines, world trade remains strong for now, and tariffs have had minimal impact on the passenger and cargo airline industries, as many other economic indicators are strong. Job creation continues, with the U.S. recording 95 months of consecutive job growth through August. The unemployment rate has stood at 3.9 percent, the lowest it’s been in two decades (see Figure 4). Interest rates remain low but have started to rise as inflation picks up. Households are recording higher net worth, and average nominal earnings are up nearly 3 percent in the past year. Fortunately, consumer confidence remains near its highest point in 18 years, as consumers have yet to be deterred by rising inflation and have yet to reduce their spending.

Oil Prices Pressuring Margins

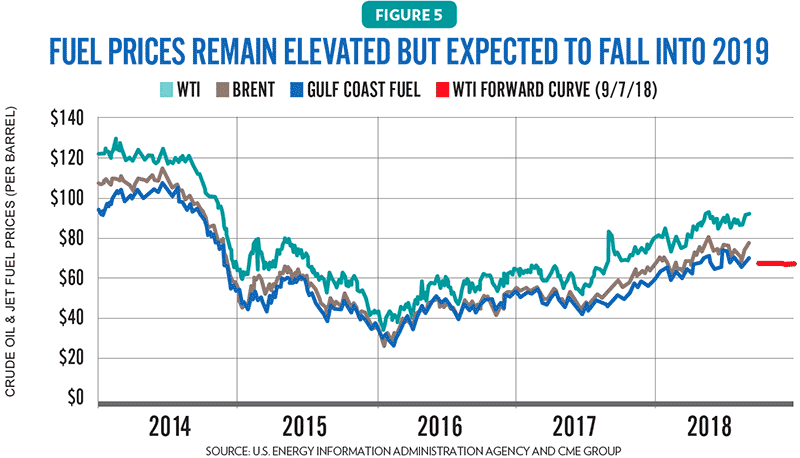

Economic growth is a key demand driver for the industry, but the price of oil also has a significant impact on the financial results the industry expects. Through August, crude oil prices increased 40 percent and 65 percent from comparable periods in 2017 and 2016, respectively. There was some downward movement in prices in late July, as most members of OPEC, Russia, and other exporting countries started to increase production. In addition, a faster-than-expected return of Libyan crude oil production following August’s unplanned supply outage could put further downward pressure on crude oil prices. Volatility can be expected to remain while supply disruption risks continue in the Middle East.

The average fuel price per gallon was up 25 percent from a year ago through the first six months of 2018, causing a $4.1 billion increase in fuel expense for the industry. While hedges can soften the impact of some of the increase, only a few airlines maintain significant hedge portfolios. Fuel has always been one of the biggest expenses for airlines; and with the significant increase so far this year, it’s now roughly 24 percent of total operating expenses. With such a significant increase in one of the largest expense categories, it’s not surprising that profit margins are being pressured (see Figure 5).

U.S. Mainline Airlines

The industry continues to generate healthy margins, but profitability is down from the last three years. Through the first two quarters of 2018, the industry posted an 8.8 percent profit margin. While this was down from 11.9 percent and 15.9 percent from 2017 and 2016, respectively, it’s still strong. The industry generated more than $87 billion in revenue through the first half of the year, with topline revenues posting a 6.5 percent increase. The increase in revenues came not only from higher ticket fares, but also from airlines’ ancillary revenue initiatives.

Ancillary revenues have fast become a permanent part of the flying experience. From basic economy fares to paying for bags, seat upgrades, front-of-the-line boarding, Wi-Fi connections, and onboard food and drink purchases, the industry has become more and more resourceful at generating additional revenue. American Airlines estimates its rollout of basic economy and premium economy products can add approximately $800 million to $1 billion in incremental revenue.

Other lucrative revenue streams come in the form of mileage and credit card loyalty programs. In fact, this source of other revenue is up 15 percent already in 2018. Delta recently commented that its relationship with American Express will drive more than $3.5 billion of additional revenue and value to the airline this year. Meanwhile, Alaska expects its mileage program to generate approximately $1 billion in annual revenue in 2018, a 17 percent compounded annual growth rate since 2013.

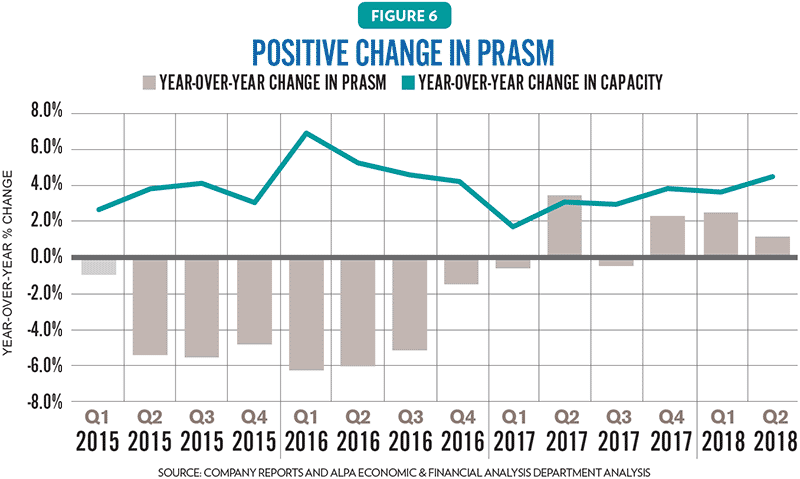

With increases in both passenger revenue and other revenue, the industry continues to post year-over-year gains in unit revenue, despite increases in capacity. Total unit revenue was up 2.1 percent from last year, while PRASM (passenger revenue per available seat mile) was up 1.6 percent, with improvements in both the domestic and international sectors (see Figure 6).

Domestic PRASM trends have increased since mid-2017, and international PRASM recently posted strong improvements, especially in the transatlantic region—which continues to benefit from strong premium cabin and leisure demand. The Latin region is seeing some stronger business demand, which should help yields; however, demand for some beach destinations has dropped due to security concerns. In addition, the residual effects of currency devaluations in Argentina and Brazil could also inhibit that region’s rebound.

Overall, total unit revenues are expected to increase approximately 2.2 percent in both 2018 and 2019, as airlines continue to focus on ancillary revenue initiatives. This is good news and will help expand margins in 2019.

CASM (cost per available seat mile), excluding fuel, for U.S. carriers increased 2.0 percent through the first half of 2018. This cost increase is slower than the increase seen in 2017 for the same period, as the initial cost increases of many of the labor agreements—such as signing bonuses—reached in 2017 won’t reoccur in 2018. In addition, as more carriers are emphasizing running smooth and on-time operations, costs related to disruptions have decreased. Keeping unit costs stable will be a challenge as more airlines look to pare capacity in the wake of rising fuel prices.

U.S. capacity was up 4.1 percent through June 2018. Domestic capacity is expected to increase 5 percent this year while international capacity is expected to grow by 2.6 percent. On an industrywide basis, total capacity is expected to be up 4.5 percent in 2018 and 3.8 percent in 2019. However, as fuel and other operating expenses rise, some airlines have reduced capacity growth for the remainder of 2018 and into 2019. But do these reductions go far enough? The lack of meaningful capacity cuts could be one reason airline stocks haven’t recently shown more pep. Investors could be concerned that oversupply could be too much in an environment of rising fuel prices, trade disputes, and political tensions.

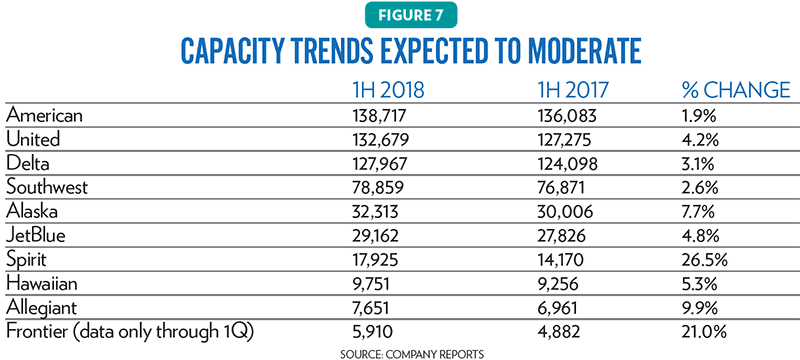

Oversupply has been one of the main reasons airlines have struggled to earn profits in an industry downturn. Airlines are using more information-technology tools to track passenger behavior. With these tools, airlines can now pick and choose which specific route and frequencies are detracting the most from overall profitability and remove these. This ability to exit failing markets and concentrate on markets of strength, thereby controlling capacity creep, should help smooth the industry profitability cycle (see Figure 7).

Canadian Industry

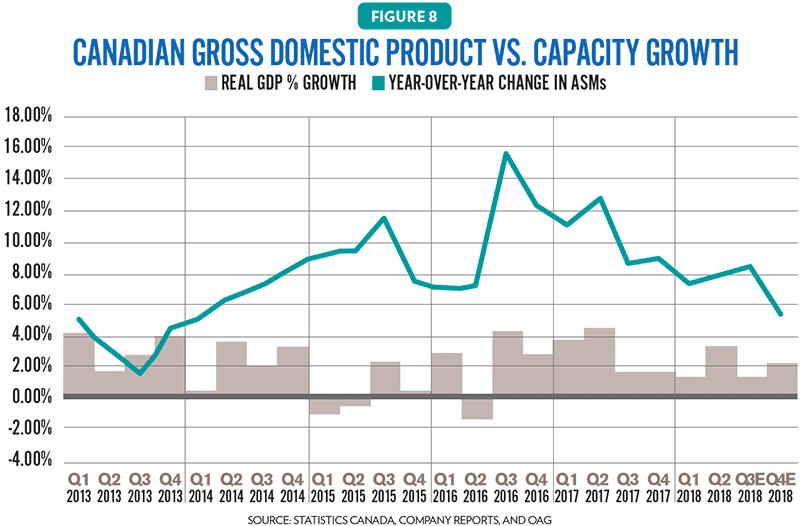

The Canadian economy has gained momentum despite concerns over U.S.-imposed tariffs. Consumer spending, wage growth, and business investment are all moving in a positive direction. While the economic growth rate for 2018 is expected to be about 2.1 percent, it’s somewhat less than the 3.0 percent growth experienced in 2017. The impact so far from U.S.-imposed tariffs on Canada’s steel and aluminum imports (industries that account for only 0.5 percent of Canadian GDP and jobs) has been relatively small. Fears over trade and the slow pace of NAFTA negotiations haven’t dissuaded Canadian companies from using their capital this year to reinvest in their businesses (see Figure 8).

For the first half of the year, results for Canadian airlines were mixed. The two largest airlines in Canada have added so much capacity that some analysts are calling it a “turf war.” As a result, insufficient pricing power coupled with rising fuel costs are leading to operating margins that are consistently lower than those of U.S. counterparts. Together, Air Canada and WestJet posted just a 2.2 percent operating margin through June 2018 (with WestJet posting its first operating loss in 13 years for the second quarter of this year), while Air Transat recorded an operating loss. Jazz Aviation saw a 9.9 percent pretax profit margin, and Exchange Income Corporation, the parent company of Bearskin, Calm Air, Keewatin, and Perimeter, had a 26.9 percent EBITDA (earnings before interest, taxes, depreciation, and amortization) profit margin. And like the performance of U.S. airlines, 2018 results were lower than 2017 for the major Canadian carriers, while Jazz’s performance was better. Exchange Income Corporation and Air Canada were impacted by a stronger Canadian dollar, while WestJet was affected by higher expenses resulting from increased capacity and the threat of a pilot strike. Jazz benefited from an increase in controllable revenue under a capacity purchase agreement; and although Air Transat posted an operating loss, it was less than in 2017 due to higher average selling prices.

The Canadian domestic market is dominated by Air Canada and WestJet. Capacity at Canada’s two largest airlines grew 7.2 percent through the first half of the year. Air Canada’s capacity growth is consistent with the airline’s objective of increasing global international-to-international connecting traffic through its major Canadian hubs. WestJet’s capacity growth is attributable to new international routes and destinations, a shift in fleet mix to larger narrowbody aircraft, and the launch of air service for both Swoop and WestJet Link in June.

What’s concerning is the amount each carrier has increased capacity above Canadian GDP growth. With Canada’s GDP expected to grow just 2.1 percent in 2018, the carriers’ 7.2 percent total capacity growth is 3.4 times that of GDP growth, and their expected 6.4 percent domestic capacity growth is approximately 3.1 times that of GDP growth. While WestJet announced a modest capacity cut for the second half of this year, Air Canada has yet to reduce capacity. The second half of 2018 scheduled system ASM growth is projected to be 6.3 percent for Air Canada and 4.2 percent for WestJet, while GDP is expected to grow only 2.3 percent in the second half of this year.

Adding to fare challenges are the new-entrant ultra-low-cost carriers trying to make a mark on the Canadian market. The latest competitor, Flair, has entered several markets out of Edmonton, Alb., and has now doubled its capacity in a year. Meanwhile, domestic capacity at smaller domestic airlines continues to grow as well. Bearskin’s scheduled capacity was up nearly 6 percent year to date in June, while Calm Air had a 7.9 percent increase in capacity. ASMs at First Air and Canadian North, which recently announced their intent to merge, were up 47 percent and 18 percent, respectively.

With such significant growth rates, it’s not surprising that the domestic fare environment is very competitive. The lack of purchasing power has many analysts questioning Air Canada’s and WestJet’s growth strategies into 2019, and the stock values of these two companies reflect that negativity.

While Exchange Income Corporation continues to post strong EBITDA earnings, the company is facing recruitment challenges and, in response, has recently implemented a pilot pathways program, which was spearheaded by the acquisition of Moncton Flight College, the largest flight-training college in Canada.

Fee-for-Departure Industry

The fee-for-departure (FFD) sector’s unique business model continues to face challenges, but there’s been some improvement in recent years. This sector’s airlines consist of two publicly traded companies, five wholly owned companies, and six privately owned companies. While all these companies compete for flying, their financial constraints are much different. In addition, because so many of these operators have constrained growth opportunities, rumors of consolidation continue.

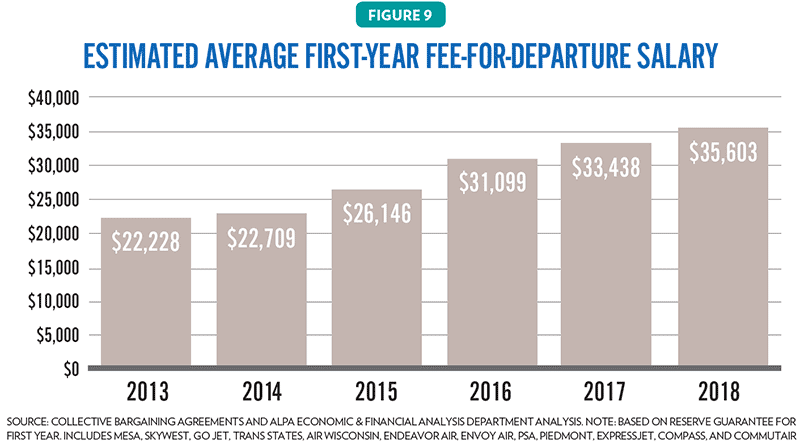

As mentioned, the industry is facing a large number of upcoming pilot retirements at major airlines. As FFD pilots move up to major airlines due to these retirements, FFD airlines are offering bonuses to attract pilots. While this has helped provide temporary relief, some FFD airlines are finally recognizing that putting money toward higher pay rates has an even greater impact on addressing pilot supply issues. In addition, many FFD airlines have established career progression paths with their major airline partners, which also helps to address pilot supply challenges. Airlines that have implemented these initiatives continue to remain competitive (see Figure 9).

FFD pilots are also starting to see some improvement in their retirement benefits. Many FFD 401(k) plans now offer upward of 5 percent matching contributions, while some have maximum matching contributions of 10 percent or more. Just four years ago, several FFD carriers didn’t offer any level of matching 401(k) contributions.

The industry continues to see the move to larger regional jets, as mainline carriers try to maintain brand quality and look to make the travel experience seamless between FFD and mainline carriers. This move to a more seamless experience includes offering premium cabins, upgraded food and beverage options, and large overhead bin space—all items found on jets with 70-plus seats.

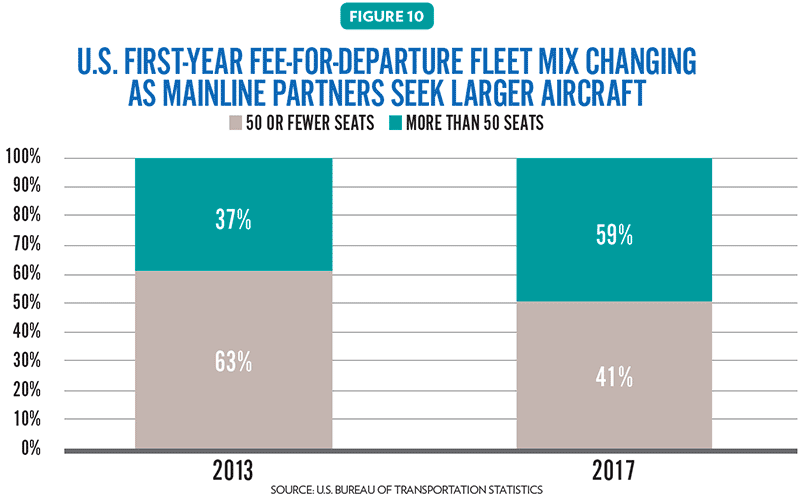

A closer look at the FFD sector shows that the fleet distribution number between aircraft with 50 seats or fewer and larger regional jets has effectively flipped. Aircraft with 50 seats and fewer represented 63 percent of the FFD fleet in 2013; last year, larger regional aircraft represented 59 percent. In 2013, the average FFD flight had 56 seats. Last year, it was 63 seats. This is a 12 percent increase in seats per aircraft (see Figure 10). This change from 50 to 70 seats will become more important in 2021, when seat limitations on regional jets are lifted at Ronald Reagan Washington National Airport, allowing airlines to add capacity without the need for additional hulls.

Recent changes in capacity purchase agreements, including extensions and new partnerships, are changing the performance results for many airlines in this sector. However, increased labor costs that are required to attract and retain pilots will put pressure on FFD carriers while they seek to remain cost competitive. In this environment, FFD airlines that have invested in aircraft themselves could face tail risk—having lease payments beyond the terms of the capacity purchase agreements. There are different options to combat tail risk, including buying these aircraft off lease, but the necessary funds to do so could be prohibitive.

Cargo Industry

Major air cargo airlines reported nearly $6.5 billion in pretax profits for the first six months of 2018. The performance in the air cargo market hasn’t fallen as much as in the passenger market. At the end of the first of half of this year, air cargo airlines posted a combined 9.3 percent pretax margin, 0.9 percentage points less than the same period in 2017, while major U.S. passenger airlines posted a combined 8.8 percent pretax margin, down 3.0 percentage points from the first half of 2017.

E-commerce and distributed manufacturing trends are creating demand for new express networks. Industry experts believe e-commerce retail sales could reach $5 trillion by 2021, up from $2.3 trillion in 2017. This suggests that demand for freight aircraft should remain strong well beyond 2021. Amazon, for example, recently expanded its Cincinnati, Ohio, hub to include space for 100 aircraft.

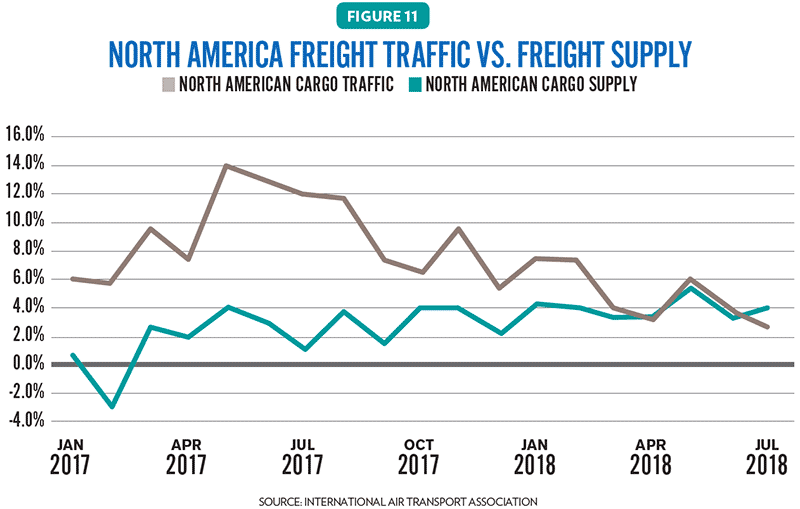

Growth in industrywide air freight traffic was up 4.3 percent year to date July 2018, while air freight capacity, measured in available air freight tons, has grown 4.8 percent year to date through July 2018. Load factors were down 0.2 percent to 44.4 percent. International load factors were slightly better at 48.3 percent. Cargo yields are up more than 16 percent from a year ago, as strong demand for e-commerce continues (See Figure 11).

Air freight volumes flown by U.S. carriers have risen at a double-digit annualized pace in the last few months. Strong consumer demand and a stronger dollar is boosting inbound air cargo. North American freight traffic is up 4.8 percent while capacity is up 4.3 percent. Asia-Pacific air freight carriers have seen a 4.0 percent increase in traffic on a 6.8 percent increase in capacity, while European carriers have had a 3.9 percent increase in traffic versus a 4.8 percent increase in capacity. Asia-Pacific, the largest air freight-carrying region—accounting for almost one-third of the global total—is most exposed to any impact from rising trade tensions.

At this point, trade impacts on U.S. carriers should be relatively small, as most of the commodities in question typically aren’t transported as air freight. In addition, ongoing economic momentum, particularly strong consumer confidence, and further signs of bottlenecks in global supply chains should continue to support demand for air freight in the near term.

Will the Industry Come Through the Next Downturn?

All sectors of the airline industry are very closely tied to economic trends. Currently, the outlook for the economy in North America is positive. Yet some issues could cloud the horizon, such as rising inflation from trade tensions and rising fuel prices, as well as geopolitical tensions. In addition, the industry needs to be watchful of its own actions that could be detrimental to financial well-being, such as excessive capacity growth.

Since the end of June, several reports from major airlines have indicated that the pricing environment is strong. This, coupled with modest capacity cuts, bodes a positive outcome for the remainder of 2018. This constant attention to fares and capacity should lead to margin expansion in 2019. If so, it would be the first time in four years that profit margins expanded.

The futures curve on oil prices shows a slightly downward trend. Whether this will materialize in fuel prices remains to be seen. Continued refleeting toward more fuel-efficient aircraft will help the industry contend with any rising oil prices, but all airlines will have to deal with the continued volatility seen in prices.

Liquidity is a good indicator of how well an airline can absorb any ups and downs that occur in the cycle, as well as any sudden shocks to the system. With more than nine years of sustained profits, many airlines have been able to accumulate strong levels of cash. Generally, airlines should seek to maintain approximately 15 to 20 percent of annual revenue in liquidity. At the midpoint of 2018, major U.S. passenger airlines had a combined $30 billion in cash and short-term investments, nearly 18 percent of annual industry revenue.

Clearly, with a strong liquidity base and information-technology tools to monitor passenger behavior, airlines can adapt to changing trends. With the ability to adapt quicker, hopefully long-term capital expenditure plans will better reflect cycle demands, so that new aircraft deliveries come during a peak instead of during a trough. Indeed, perhaps the previous cycles of recovery, expansion, descent, and contraction will be replaced with moderate growth, moderate expansion, little descent, and no contraction.